Going From Good to Great Credit Takes These Power Moves

Do you have good credit? You do, according to most creditors, if you possess a FICO score between 680 and 739.

But if good credit is good, excellent credit is even better. This article explains, “What is an excellent credit score?” and how to improve credit score factors that affect your borrowing costs.

Find a personal loan to raise your credit score

What is a good credit score today?

The major credit bureaus — Experian, TransUnion and Equifax — do not tell lenders if your FICO score is “good” or “fair” or “poor” or “excellent.” Those are judgments that creditors make, and not all creditors define a given score in the same way.

However, there are common conventions. For instance, many creditors consider your credit score to be “good” if it falls between 680 and 739. As of this writing, the average FICO score in the US is 700, a good score.

Lenders generally place FICO scores of 740 or higher in the “excellent” category.

If you already have good credit, taking steps to raise credit score numbers to excellent can really pay off. You clearly manage debt pretty well, and a few improvements may give you excellent credit without much trouble.

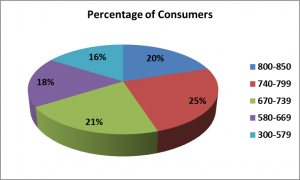

The chart below shows how FICO scores are distributed across the population. the average FICO as of this writing is 704.

How much can you save with excellent credit?

Approximately 25 percent of the US population has “excellent credit,” according to the National Association of Realtors (NAR). Consumers with excellent credit receive more credit opportunities, and it costs them less to borrow.

Here is how much you might save by when you improve your credit score from good to excellent.

Related: personal Loan Interest Rates (How to Pay Less)

Mortgage rates

According to data from FICO, an applicant as of this writing with a good 680 score qualifies for an APR of 4.246% for a 30-year fixed-rate mortgage. For a $300,000 loan, that’s monthly principal and interest of $1,475.

An applicant with an excellent 760 score pays 3.847% ($1,406 per month), saving $69 per month and $24,840 in interest over the life of the loan.

In addition, those with better credit scores may be able to finance with lower down payments. And applicants with better credit scores also pay lower mortgage insurance rates. One national mortgage insurer charges a borrower with a 760 FICO score .28% for mortgage insurance with 10% down. But an applicant with a 680 score pays .65% — over twice as much!

Auto loans

The difference between auto financing rates for consumers with good credit and those with excellent credit is seriously wide.

According to MyFICO, auto buyers with 60-month loans pay 8.391% with a 680 FICO, but that drops to 6.11% when they improve credit score ratings to 690 (just ten points!) and plunges to 4.773 with FICOs of 720 or better.

If you finance a $30,000 car over five years, going from 680 to 720 or better could save you more than $3,000.

Credit cards

Credit card interest rates are highly-dependent on your credit score because the loans are unsecured. Your credit history is statistically a good predictor of how you’ll pay a new account, and lenders charge more for riskier accounts.

Consumers with good credit generally qualify for credit cards with interest rates in the 14% to 17% range. But with excellent credit, that falls to a range of 10% to 13%.

For a $10,000 balance, it would take 36 months paying $323 to clear it, costing $1,628 in interest at 10%. For the same loan at 14%, your payment increases to $342 and your total interest to $2,312.

Related: Why Personal Loans Beat Credit Cards for Large Purchases

Personal loans

Personal loans, like credit cards, are unsecured. So your credit rating has a huge impact on your interest rate.

For online personal lending sites, offers to consumers with the best credit range from 6.46% to 8.81%. Applicants with good credit get 10.33% to 13.80%.

Financing $10,000 over five years costs you $1,117 more if you pay 10.33% instead of 6.46%.

credit: How to raise your credit score

Raising your credit score from good to excellent probably requires less effort than you think. Follow the steps below and monitor your score. Seeing it improve can be really motivating, so check it a few times a year.

Payment history

Payment history comprises 35% of your FICO score. You can’t have excellent credit if you pay late — period. In fact, one late mortgage payment can do more damage to you (60-80 points!) when your credit is good than it does to someone in the fair or poor range.

FICO, the company that creates the most widely-used scoring models, lists the characteristics of credit superheroes:

No missed payments: 96 percent of those with excellent credit show no missed payments on their credit history. The bad news? It takes about four years after missing a payment for your scores to return to the highest level. The good news? If you have a good history with a creditor, and you contact it and beg convincingly, it may remove the late payment from your credit history.

Lengthy credit history: Consumers with excellent credit usually have long credit histories. In fact, people with the best credit scores don’t open new accounts that often and on average, their accounts are 11 years old. While you can’t make time go any faster, you can take steps to keep your account age long. For instance, request a larger line of credit from an existing issuer instead of opening a new account.

Use of credit: High scorers carry an average of seven credit cards, four with balances. And about one-third owe more than $8,500 in revolving debt. That does not necessarily mean that they carry balances from month-to-month, however. Carrying balances harms a more important factor — utilization.

Rare blemishes: About one percent of high achievers have a collection listed on their credit report. But just one in 9,000 shows a tax lien or bankruptcy. And these are likely to be old, not recent. The good news is that it is possible to have high credit scores after major derogatory events, if you’re willing to do the rehab work.

Credit utilization

Almost as important as your credit history is your “credit utilization” ratio. That’s the amount of credit you’re using divided by the amount available to you. Utilization makes up 30% of your FICO score.

Consumers with good credit scores don’t generally use more than 30% of their available credit. But those with excellent credit often use no more than 10%.

Can you reduce your utilization by opening up more credit cards? Sure. But you reduce the average age of accounts and increase the number of inquiries. And that may drop your score, at least temporarily.

It’s different if you only have one or two cards, and / or your credit history is short. In that case, adding another account can help. FICO’s data show that consumers who max out their only card are more likely to miss future payments, so having too few accounts can hurt you.

Asking your current creditors to increase your credit limit is usually more effective for dropping your utilization. Or try a personal installment loan to clear all of your credit card balances and pay off your revolving debt altogether.

Related: Advantaged of Using Personal Loans to Pay Off Bills

Inquiries

To earn the highest credit score you can, don’t apply too often for credit.

Just one inquiry can cause a five point drop in your credit score. While FICO won’t penalize you for rate shopping an auto loan or mortgage, too many inquiries for other accounts can do damage.

Why should creditors care how many inquiries you have? Because they can indicate that you’re getting in over your head. FICO research found that you’re eight times more likely to declare bankruptcy if you have at least six recent inquiries than consumers with no inquiries on their reports.

To minimize inquiries, only apply for credit when you need it, and stay away from offers geared to people with better scores than yours. If you have good credit, but you apply for credit cards for excellent credit, you might get turned down repeatedly. And you’ll have those pesky inquiries dragging you down.

Protect excellent credit

Once you earn an excellent credit rating, expect to be showered with love by all kinds of creditors. But don’t let your new-found excellence go to your head. Too many accounts or owing too much can drag your FICO score back down. If you consolidate credit card debt into an installment loan, don’t make the mistake of running your credit card balances back up.

Consumers with the best credit scores use their accounts conservatively. And they are rewarded, because it’s true that lenders prefer customers who don’t need the money.