Want a Lower Personal Loan Rate? Here’s How to Lock It In

Used responsibly, personal loans can allow you to get the things you want today without waiting. But what interest rate will you pay? Is it worth it to get a personal loan? Personal loan rates depend on three factors:

- Your credit score/credit grade (better credit gets you better rates)

- The term of the loan (longer terms come with higher rates)

- The loan amount ($10,000 to $25,000 seems to be the “sweet spot” for the best personal loan interest rates)

To find the best personal loan interest rate available to you, shop with several competing providers. Interest rates can vary widely between competitors for the same loan.

How Personal Loans Work

For lenders, personal loans are both attractive and risky. The attraction is that personal loans earn higher interest rates than secured financing. The risk is that if the borrower elects not to repay the loan, the lender may have a hard time collecting.

Personal loans can generally be divided into two categories. Revolving loans are a form of financing in which you can borrow and pay back as often as you like up to a given amount of credit. Personal lines of credit are revolving loans.

The other, more common type of personal loan is the installment loan. Installment loans deliver a lump sum, a (usually) fixed interest rate and regular monthly repayment. Example: Borrow $1,000 at 6% interest for one year, and you make 12 monthly payments of $86.07 per month.

That’s a total repayment of $1,032.80. the $32.80 is your interest charge for the life of the loan. Other loan costs can include origination fees (also called set up charges). These can range between one and five percent of the loan amount. So if you paid a 3% origination charge, your total costs would be $62.80 to borrow $1,000 for one year.

Find Low-Rate Personal Loans

Research personal loans to find the best interest rates and quickest funding. Use the tool below to see which loans best suit your situation.

Personal Loans and Interest Rates

One very good way to understand personal loan costs is to look at the monthly figures published by the Federal Reserve. The information is generally a few months behind, but give us a good idea of market costs. As of this writing, the latest Fed averages look like this:

- The average personal loan interest rate for 24 months was 14.32%

- Credit card borrowers paid 22.76%

- A 60-month car loan cost 6.73%

Note that these are averages in the recent past. Not today’s date. How much will you pay? You probably won’t pay the average rate. It will likely be more or less, depending on your credit grade.

Credit Grades

We generally think of letter grades as being “A,” “B,” “C,” etc. You can certainly find references to “A” credit or “B” credit, but in each case these are subjective terms. They can mean whatever someone wants them to mean. What really counts, plain and simple, is your credit score. Higher is better, and lower can be a problem.

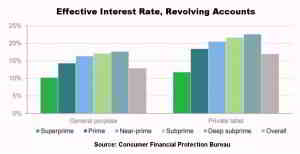

Some lenders may see a top borrower as someone with a 760 score, while other lenders might want 800. A study by the Consumer Financial Protection Bureau found that the real cost of consumer borrowing (called the Total Cost of Credit, or TCC) varied substantially depending on credit standing.

The Bureau divided borrowers into five groups. If you look at the table below, you can see that there’s a substantial difference between the interest rates paid by those with strong credit and those without.

Looking at general purpose credit card lending, we can see that some borrowers pay a lot more than others.

As a borrower, you very much want to be in the “super-prime” class. If this was a movie, your superpower should easily get low interest personal loans.

Prime and near-prime borrowers pay more. And subprime and deep subprime applicants pay significantly more — if they get approved.

Again, note that these are averages and the credit buckets are fairly large and general. And these interest rates are for credit cards. Personal loan providers generally charge lower interest rates than credit card issuers for the same credit grade. Individual personal lenders can have over 20 credit tiers, and their personal loan interest rates can range between 5% and 40%.

Term

All other factors being equal, the longer the borrow, the higher your interest rate. That’s assuming that you choose a loan with a fixed interest rate. This applies to other loans like auto financing as well. Here are personal loan interest rates as of this writing for one national credit union:

1 to 2 years: 8.5% to 13.5%

2 to 4 years: 9.5% to 14.5%

5 years: 10.5% to 18%

You can minimize your interest rate and your total loan cost by choosing the shortest term you can afford. Assuming that you’d qualify for the best interest rate with that credit union, here’s what your total interest cost would be to borrow $1,000:

How to Compare Personal Loan Costs

When you get an offer from a personal lender, look at all of the fees as well as the interest charges. That’s not actually hard.

- Multiply the monthly payment by the months in your term to get the total you’ll pay over the life of the loan

- Subtract the amount you are borrowing

- Add any origination, setup, maintenance or other charges

Then just choose the loan with the lowest overall costs.

Another way to compare that works better for revolving personal loans or those with variable interest rates is to look at the annual percentage rate, or APR. In general, the loan with the lowest APR is also the one with the lowest combined upfront costs and interest charges.

How to Lower Personal Loan Costs

The big issue for borrowers is how to lower personal loan costs. There are several steps you can take to get a better deal.

- First, check your credit reports to assure there are no errors or outdated information. You can get one free credit report every 12 months from each of the three major credit reporting agencies — Experian, TransUnion, and Equifax — by going to AnnualCreditReport.com.

- Second, boost your credit score by paying bills on time and in full. You’ll also avoid late fees this way.

- Third, create a budget — and learn to live within it. You can likely avoid high-cost payday lenders and auto title lenders by having just $400 in the bank for emergency costs.

- Fourth, don’t just look at only the interest rate. Consider the origination charges. In the example with the $1,000 loan, the interest was $32.80. But the origination charge nearly doubled the cost of the loan.

- Last, and perhaps most important, compare offers from several personal loan providers. Interest rates and fees vary widely for all credit grades, and the more offers you see, the better your chance of getting a good deal — no matter what credit grade you find yourself in.