Tie the Knot Without Tying Up Your Finances

Your first question, once you decide to get married, may be how to pay for your wedding. Planning and paying for your wedding in advance offers important advantages:

- Popular venues may be booked a year ahead of time, especially in the summer (get what you want by booking early)

- You may be able to save money by reserving and paying early

- You can pay off a good portion of the bills before your ceremony

- More time means less hassle — your wedding should be fun, not stressful

Here’s what you need to know about wedding planning and how to pay for a wedding. So you can enjoy your big day with family and friends.

This blueprint for wedding planning is designed to provide ample lead time and save money.

12 to 18 months before your wedding

As far in advance as possible, take care of the following six tasks:

- Create your budget, determining how much money you’ll be able to spend, and where you’ll get it (family, a personal loan, crowdfunding, etc.)

- Choose your wedding party and consider your guest list

- Select your date and venues (many venues require a 50% deposit upfront)

- Book your officiant

- Research decor, bands, caterers and florists (or hire a planner)

- Have your engagement party

6 to 12 months ahead of your wedding

By now, you may have finished paying for your venue deposit and might even begin saving for the remaining balance. It’s time to handle the following ten items:

- Buy a dress (deposit 50%)

- Book entertainment (deposit 50%)

- Book caterers (deposit 50%)

- Hire photographer

- Register for gifts

- Set up your wedding web page

- Reserve hotel block rooms for out-of-town guests

- Buy invitations

- Order bridesmaids dresses

- Book a florist (50% deposit)

- Book transportation

Related: Personal Loan Interest Rates (How to Pay Less!)

4 to 6 months in advance of the wedding

With many deposits already paid, there are still nearly a dozen important wedding details to cover:

- Buy wedding rings

- Go through ceremony with officiant, and write your vows if desired

- Order party favors and printed programs and menus

- Review plans with vendors

- Organize extras such as seating, electricity and bathroom facilities, if needed

- Book rehearsal and rehearsal dinner venues

- Order your cake (50% deposit)

- Pick your music

- Buy wedding shoes and underwear, start dress fittings

- Schedule hair, makeup and nail professionals

- Coordinate with bridal shower host

2 to 4 months ahead of your ceremony

Use this time to save for all remaining costs, as much as possible. Your task list includes four recommendations:

- Meet with photographer

- Send invitations

- Meet with deejay or band, choose playlist for first dance etc.

- Send announcement to newspaper

1 month before the wedding

Final payments to vendors can be a significant expense. If your savings aren’t sufficient, this is when borrowed funds may be helpful.

- Get final count from RSVPs

- Send rehearsal dinner invites

- Create seating chart

- Get your marriage license

- Have final fitting for wedding dress

- Make final payments to vendors

- Confirm with hair, makeup and nail pros

- Provide directions to all drivers (limos, deliveries, etc.)

- Buy bridesmaids gifts

1 week ahead of the big day

Prepare your team so you can have a fantastic time on your wedding day.

- Reconfirm with all vendors

- Pick up dress

- Communicate to bridal party where to be and when

- Pack for your honeymoon

- Break in shoes

- Delegate someone to run interference for you on your wedding day

How to pay for a wedding

You probably noticed that there are a lot of payments on your schedule, and that many service providers want hefty upfront deposits. This may be alarming if you expected to pay as you go. However, it’s manageable if you break it into several steps.

What is your wedding budget?

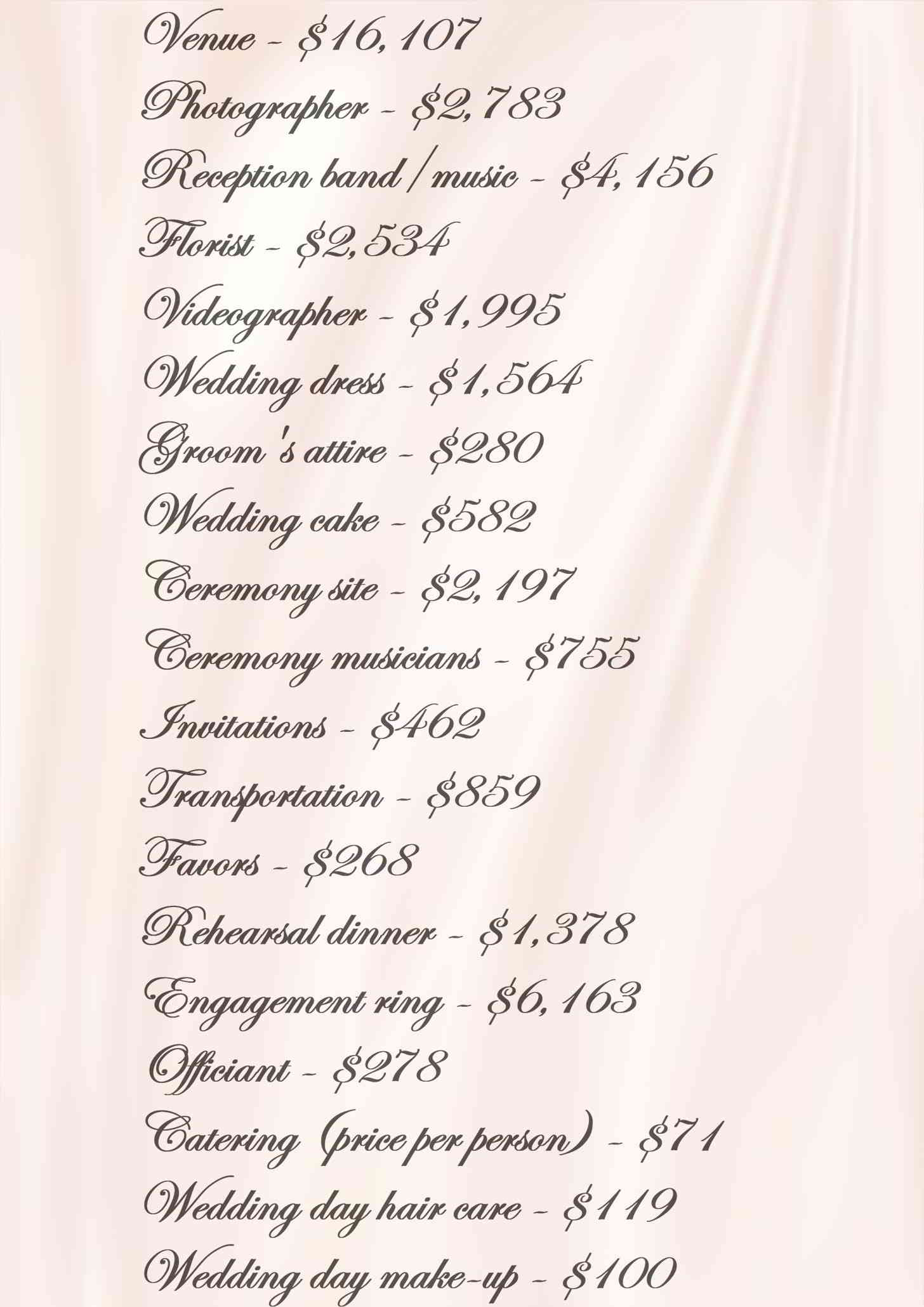

According to the latest Brides American Wedding Study, the average U.S. wedding costs $26,522 for 135 guests. Nearly half of couples paid the entire cost themselves. But one-third exceeded their budgets — not the best way to launch a happy marriage.

To set your budget, look at three sources of cash:

- Your savings

- Gifts

- Your income (borrowing power)

Once you know how much you can spend, you can adjust your expectations accordingly. Experts advise leaving a 10% cushion so you don’t run into problems being unprepared for higher than expected bills.

Paying for a wedding should not take decades

Once you have a budget, it’s time to determine how to pay for a wedding. If you can get a credit card with a zero interest introductory rate or a great rewards program, that’s a convenient way to make those deposits. But average credit card interest rates are often high — on average about 78% higher than average personal loan interest rates.

And if you base your budget on the required minimum payment, you might still be paying for your wedding when your first child is graduating high school!

Related: Personal Loans Beat Credit Cards for Large Purchases

Paying for your wedding with a personal loan

A better way to plan your borrowing is to calculate what you can afford to pay each month. Your credit rating determines your interest rate, and your interest rate drives how much you should be able to borrow at a given payment. Ideally, you want a loan that you can pay off before your wedding day, so you can start your life together without much debt.

For example, if you have $5,000 in savings and anticipate gifts from parents, friends and family to total approximately $10,000, you may need to borrow close to $11,000 to pay for an average wedding (135 guests) costing $26,000. if you can afford $600 a month, and your wedding is 18 months away, the amount you can borrow at various interest rates looks like this:

You might combine a personal loan with credit card financing if that allows you to access some great rewards (perhaps travel for your honeymoon?) or take advantage of zero interest. For instance, if you qualify for a 12 month interest-free introductory credit card offer, and can afford a $600 monthly payment, you might can borrow a little more, at a lower cost.

- Instead of $10,304 at a 6% interest rate, you can borrow $10,738 with the same payment

- Pay $600 a month for 12 months at zero interest, which should knock $7,200 off your balance interest-free

- Finance the remaining $3,538 over six months at 6%, paying $600 a month

Using this strategy allows you to finance $10,738 and pay just $62 in interest.

Alternatively, you can charge your wedding costs on your rewards card and pay that off with a personal loan.

If possible: start your life together debt-free

Wedding planning should include financing, because these choices impact your life long after the last song has played and your flower girl has fallen asleep covered in frosting.

Think twice before spending more than you can afford to pay off quickly. Most financial experts don’t recommend long-term financing for short-term objectives. And while your marriage will hopefully last a lifetime, your wedding is over quickly. You don’t want to be stressing about money while adjusting to married life.