Vantage and FICO Scores in 2024: How They Impact Your Loan Interest Rates

Vantage and FICO scores are the big names in credit reporting today. So, what are the differences between VantageScore and FICO? And how do those differences affect your borrowing?

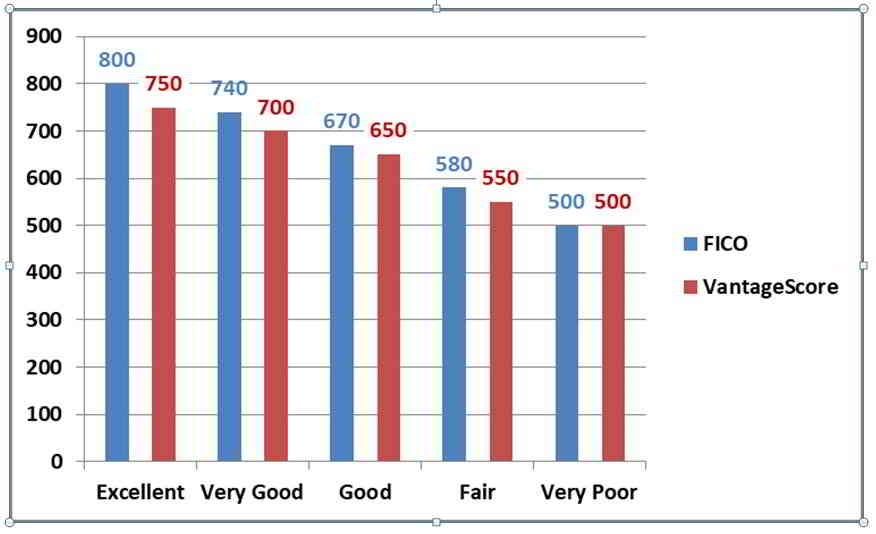

What Are Credit Scores?

Your credit score represents your desirability as a borrower — mathematically distilled to a three-digit number designed to predict your likelihood of repaying your loans.

In 2019, there are two major credit scoring systems fighting for turf and territory — FICO and VantageScore.

What Is a FICO Score?

Established in 1956 by Bill Fair and Earl Isaac, the FICO model “introduced analytic solutions such as credit scoring that have made credit more widely available, not just in the United States, but around the world.”

The FICO score incorporates five factors, weighted by importance. From big to small they are:

35% – Payment history documents if you pay bills in full and on time.

30% – Utilization ratio is your credit used divided by your credit limits. FICO likes lots of unused credit. If you have a $10,000 line of credit and use $1,000, that’s good. If you regularly have $9,800 outstanding, your score will go down.

15% – Length of credit history indicates that longevity is a plus with credit scoring. Alternatively, if you are new to the credit world, you have not had time to develop a “thick” credit report with lots of references.

10% – What is your credit mix? The scoring system values consumers who use a variety of credit accounts such as both revolving credit for credit cards as well as installment credit with accounts that require regular monthly payments such as mortgages and auto loans.

10% – Are you opening new credit accounts? A quick increase in credit accounts is a red flag. Does the consumer need new lines of credit because of financial problems?

What Is a VantageScore?

Introduced in 2006, this model was developed by the three largest credit reporting agencies (CRAs), Equifax, Experian, and TransUnion. Today, the model is operated by VantageScore Solutions, “an independently managed firm responsible for maintaining, revalidating, and updating the scoring model and providing educational resources for lenders and consumers.”

The VantageScore formula is different. Here, in order, are the most to least important factors.

- Total credit usage, balance, and available credit (that’s called utilization in the FICO system)

- Credit mix and experience

- Payment history

- Age of credit history

- New accounts opened

Note that payment history, the most influential factor for FICO, comes in third place with VantageScore.

More than 1 score

There is no single “credit score” but rather dozens of scores depending on the lender’s purpose. Lenders might use one score for mortgages and another for credit cards, car loans, and general purposes.

Reporting errors can cause complications because your credit score depends on your credit report. If your credit report has factual errors or items which are out-of-date, your score drops. That can mean higher interest rates and maybe even a loan denial.

Credit reporting errors can cost you

A 2013 study by the Federal Trade Commission found that “one in five consumers had an error on at least one of their three credit reports.” About one in 20 consumers had a credit report error that changed scores by at least 25 points and a few reports had so many mistakes that scores changed by more than 100 points.

Since every credit score point counts, it pays to check credit reports for mistakes and old items. You can get one free copy of your credit report every 12 months from each of the three major credit reporting agencies (CRAs) – Equifax, Experian, and TransUnion – by going to AnnualCreditReport.com.

Bank account monitoring

In recent years, the credit scoring process has been changed with new and better ways to handle medical billing and financial liens. This year, the new innovation is bank account monitoring.

If you agree — and ONLY if you agree — the movement of money in and out of your bank account can now be electronically tracked with the UltraFICO and Experian Boost programs. By revealing bank account transactions, say the credit bureaus, consumers can get better credit scores.

According to Fair Isaac, “seven out of 10 consumers who exhibit responsible financial behavior in their checking and savings accounts could improve their score.”

For those with marginal credit scores, the new programs might help you get better financing. Alternatively, if privacy is a concern, then maybe bank monitoring programs are not for you.