Budgeting Doesn’t Have to Stink – Make It Work And Be Fun

There could be many reasons why you’re here, reading this. Perhaps you’re desperate and ducking calls from collection agencies. Maybe you have a new goal and need to save for something joyous: a baby, a wedding, your first home, or a new car. Or perhaps you’re facing a new challenge: sickness, fewer hours at work, or a new job in the gig economy. Whatever your motivation, you realize you can take back control of your life when you set up a budget.

This article will show you:

- How to create a budget

- How to stick to a budget

- That having a budget won’t suck all the fun out of your life — it’ll make it better and more enjoyable

Bet that last one had you raising an eyebrow. But it’s true.

Life Is Better on a Budget

It’s fun to buy expensive things. And there are times when you’re feeling down or have had a tough week and you want to treat yourself. None of that needs to stop just because you’ve set up a budget.

What should stop is buyer’s remorse: that sinking feeling you get in the pit of your stomach after the high of making an extravagant purchase. You feel remorse because you’re realizing the financial implications of your purchase and are worried you’re storing up trouble for yourself down the line.

And that really does suck the joy out of buying stuff.

The Joy of Spending

If you work within a budget, you’ll no longer feel buyer’s remorse, at least over the financial aspects of your purchases. Writing an article on buyer’s remorse in Psychology Today, Harold Sigall Ph.D. explains why: “On the simplest level, if our choices are informed by trustworthy data, we increase the chances of good outcomes.”

Your budget provides those “trustworthy data” that increase your chance of a good outcome. And that means you can enjoy the things you buy without that feeling of dread. But there’s better yet news: you can buy more and better goods and experiences on a budget.

You Can Buy More When You Budget

Having a budget doesn’t mean you get to buy fewer or cheaper goods and treats over your life. It means you get to buy more and better ones.

That’s because you’re likely to spend more of your own money on yourself — and hand over less of it in interest, fees, and charges to banks, credit card companies, and other lenders. Of course, you can still borrow when you want or need to.

But you should do so in a better informed and more mindful way. And that means you’re probably going to borrow less.

Better yet, with your finances under control, you may well end up with a better credit score. So you should pay a lower interest rate when you do decide you want a mortgage, loan, or credit card.

How to Create a Budget

Don’t believe the financial fundamentalists who pretend there’s only one way to set up a budget. You have loads of choices. And the important thing is that you find one that suits you.

By all means, try one out and then switch to another if the first doesn’t work for you. Your budget is there to serve you. You’re not supposed to be its slave. So don’t resist too much if your personal budgeting techniques evolve.

You can choose from a range of technologies: from pen and paper, through spreadsheets and envelopes (no, really) to the latest smartphone apps. We’ll come on to those later. But, whichever you select, there are some suggested rules that might help you.

Related: How to Save a Down Payment for a House

Start strict

It’s a good idea to start off with a clear, high-definition picture of your spending. And that involves tracking literally every cent you spend.

Of course, you don’t have to do that for the rest of your life, unless you find it helpful. But starting out with that level of granularity can be seriously useful, perhaps for the first couple of months. And you might want to take new, detailed snapshots of your spending every year or two to stay current with your evolving lifestyle.

It all adds up

The problem with very small expenditures is that they feel like nothing. But, taken together, they add up. And you may be surprised by how much your daily newspaper or coffee is costing you when you multiply their prices to find what you’re paying on a monthly or annual basis.

Of course, what you do next is your choice. You may feel your coffee, newspaper, or whatever is well worth the cost. Or you may choose to take a Thermos to work and to get your news online.

Set goals

Whether you are saving for an event, to buy something, to get out of debt, or fund a happy retirement, it can be helpful to set yourself cash targets and solid time frames.

“I want a down payment of $x dollars within three years.” Or “I need $y in time for my golden wedding anniversary to pay for a dream cruise with my spouse.” Or just, “I want $z in an emergency fund within four years so I can weather any period of sickness or unemployment or reduced hours — and feel less vulnerable.”

You may want to accumulate a particular sum by a particular date so you can start a business or either start or expand an investment portfolio. Setting a date and amount increases your chance of success.

Related: Sinking Fund (Why It’s the Best Way to Save)

When “saving” isn’t saving

Your objective may not be, at least initially, to see your savings account balance rise or your investment portfolio expand. If you are carrying high-interest debt, you should probably be putting all or most of the savings your budgeting generates toward paying those down.

After all, it doesn’t make much financial sense to put money into a savings account with perhaps a 2% yield while you’re still paying close to 20% APR on credit card balances. So, unless you’re saving for something special, use your budget to pay down expensive debt first.

Next: Set milestones

Now you have your goal in place, you can set yourself milestones. These are tactical objectives that let you know whether you’re on track to achieve that goal.

For example, let’s suppose you want to save $44,000 for your wedding in four years’ time. (Incredibly, that $44,000 was the average cost of one in 2018, according to Brides.com.) You’ll want to save $11,000 a year, which is $917 a month.

So now you have a target and your monthly milestones provide a way for you to measure your progress. But are they realistic? Can you save as much as you need within the time you have? If not, you may have to scale back your wedding plans (or whatever) or delay it so you have longer to save.

Related: How to Plan and Pay for Your Wedding

How to Stick to a Budget

Perhaps the biggest points of having a budget are to help you be mindful of money and to enable you to make informed financial decisions. It is, in Dr. Sigall’s words, your source of “trusted data.”

But you have to use it as a source. And that means monitoring it regularly, at least once a month. If you use a more traditional method of maintaining your budget (pen and paper or a spreadsheet), you’ll do that automatically every time you update it.

But some recent smartphone apps automate the process to such an extent that your involvement is limited. That’s great for saving labor. But, with some of those, it can mean you don’t have to regularly review your progress or notice whether you’re reaching your milestones.

If you automate your budget, schedule time, perhaps with the help of a recurring calendar prompt, to study the figures and make sure you’re on track.

Milestones can vary

All miles are the same. They’re 5,280 feet long. But, when it comes to budgeting, months are often different.

So, for instance, you may not be able to save as much in the month of the holiday and the one when you’re on vacation. Returning to our wedding example, perhaps you’re able to save $500 less each August and December.

That’s fine. Just bump up your saving during easier months to make up the $1,000 shortfall. That works out at $100 more for each of those 10 easier months.

Of course, this works the other way, too. So, if you’re lucky enough to have a job that pays a worthwhile annual bonus, you may be able to save way more during the month you get that. The same goes for regular tax rebates. If you can rely on both or either of those, you need to put aside less during other months. So build them into your savings timetable and space your milestones accordingly.

Expect to fail

You need to manage your own expectations. Unless your life is exceptionally predictable and serene, you’re almost bound during some months to fail to meet your savings target.

Whether or not you beat yourself up for that failure will depend on why it happened. If you made some silly impulse purchase of something you didn’t need, then maybe you should feel guilty. But if you were faced with some unavoidable, necessary expense (the car broke down, perhaps, or you had a healthcare issue that cost you), then you really mustn’t feel bad. Either way, simply do your best to catch up by some future milestone — and not necessarily the very next one.

Even if your failure was down to a personal weakness, you should just dust yourself down and resolve to do better. Think of yourself as a recovering spendthrift. You’d be unimpressed if a friend who was a recovering alcoholic quit AA just because she’d been on a bender. You need to see your saving and budgeting regime in the same way: to err is human.

Learn — and evolve your budget

If you never or rarely hit your milestones, and find you’re consistently falling behind with your targets, you need to ask yourself why. It might be because you’re not taking the process seriously enough and need to be more self-disciplined.

But it might also be that you’ve set yourself unrealistic targets. By now, you should be able to recognize the gap between your income and unavoidable outgoings. In fact, once your budget is up and running, you should be able to put a figure on it. So look at that high-definition picture of your spending that you made when you first started budgeting (or make a new one if things have changed) to see if there’s room for more cuts. If there isn’t, consider changing your targets to make them more realistic.

Of course, how much you can change those targets will depend on how flexible your personal circumstances allow you to be. So you may be willing to delay a purchase or vacation to give yourself the time you need to save enough comfortably. You may even be willing to borrow using a personal loan to keep your plans on track, though that rather defeats the object of your saving.

Related: Personal Loans beat Credit Cards for Large Purchases

Targets when times are tough

But suppose your budget is there to help you fight off collection agencies. Suppose you’re desperate.

Again, you might be able to borrow with a debt consolidation loan that reduces your monthly outgoings. But, if that’s not an option, you may have to find further cuts in your spending, even if they cause you pain.

And, if that’s simply not possible, you may need credit counseling. Just make sure you avoid the sharks and find a reputable counselor. According to the Consumer Financial Protection Bureau, good sources for those include the websites of the Financial Counseling Association of America or the National Foundation for Credit Counseling.

Targets when times are easy

What do you do if you’re reaching every milestone without breaking into a sweat? Well, immediately after offering up a prayer of gratitude to your God, you should ask yourself some questions, including:

- Do I need to make my savings goals more challenging?

- Should I be using these good times to give myself better protection against possible bad ones in the future?

- Is my emergency fund healthy enough?

- Am I on track for a comfortable retirement?

- Am I missing out on profitable investment opportunities because I don’t have the cash on hand to buy into them?

Remember, your budget is there to serve you, not the other way around. But, if you chose to answer Yes to any of them, you may want to set yourself new and higher objectives, goals, and milestones.

Related: Good Debt, Bad Debt (When to Borrow and When to Save)

How Every Budget Works

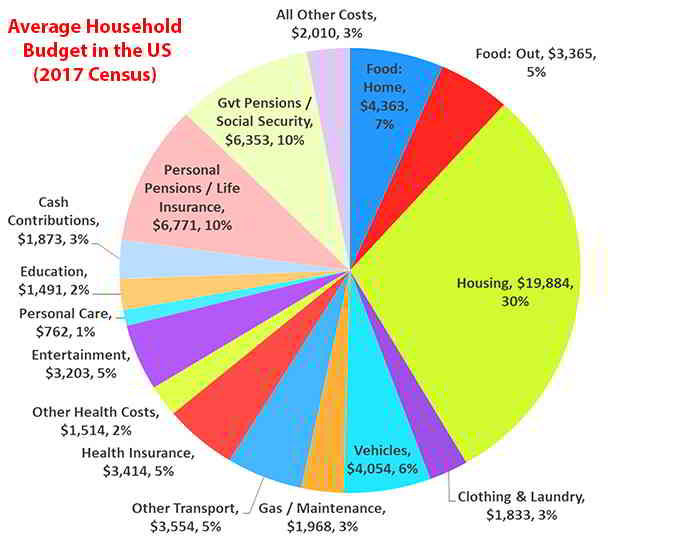

Regardless of which method or software you use to set up your budget, it’s going to break down your income and your outgoings so that you can actively manage the gap between the two.

Here is the average budget for U.S. households, courtesy of the Census Bureau:

Income

For many of us, our incomes are pretty much fixed. We receive a regular salary, pension or welfare payment (perhaps plus alimony or child support) that rarely varies. True, we could ask for a rise, take a second job, rob a bank or sell one of our children into slavery. But most of us can’t increase our incomes at will. So almost all our focus is going to be on the expenditure side of our budget ‘s (real or metaphorical) ledger.

It may be a little different for some of the rest of us. If you largely rely on commissions or performance pay, or are self-employed, work in the gig economy or are a freelancer, you may be able to influence your income by working longer or harder. So you’ll likely pay attention to the income side of that ledger as well as the expenditure side.

Expenses

Household budgets traditionally differentiate between “fixed” (inescapable) expenses and discretionary spending. It’s easy to nitpick over the definitions, but here’s what they usually mean.

Fixed expenses

These are costs that you can’t easily avoid or change, including:

- Rent/mortgage

- Property taxes (if you pay them)

- Homeowners’ Association (HOA) fees (ditto)

- Insurance premiums

- Payments on existing loans (student, auto, personal …)

- Minimum payments on credit and store card balances

- Child support

- Alimony

Of course, these aren’t all completely inescapable. You could save on several of them simply by moving to a less expensive home. And they’re far from fixed: many go up at least annually. Still, they’re not things you can change easily month-by-month.

Discretionary spending

Just as fixed outgoings aren’t totally fixed, discretionary spending isn’t wholly discretionary. It’s just easier to control.

So, for example, food counts as discretionary, even though your stomach might disagree. It’s the same for gas, even though you may absolutely need that to get to work. The point is that it’s easier to change (by skipping your regular Sunday lobster or not driving across the state to enjoy a view) than fixed expenditures.

So everything that doesn’t count as fixed is discretionary. And it’s where you’re most likely to find opportunities to cut your costs.

Discretionary spending categories

Within your budget, you’ll categorize each expenditure under an appropriate heading. Those might include:

- Groceries

- Personal care (salons, beauty products, personal hygiene products)

- Gas

- Eating out

- Wine, beer and spirits

- School expenses (lunches, trips, uniforms, books …)

- Health care

- Fitness (gym membership, sports and fitness equipment and clothing …)

- Car maintenance

- Entertainment (cable tv, theater trips …)

- Utilities

- Clothes (purchases and dry cleaning)

- Shoes

- Home maintenance

- Home purchases (appliances, furnishings, accessories …)

- Commuting costs (if you take trains or buses)

- Gifts

- Walking-around money (see below)

You may not need all those categories. Or you may need some more. You tailor your budget layout to your lifestyle. So, for example, if your personal care regime runs only to toothpaste, soap, shampoo, and deodorant, you might want to lump those under groceries.

Discretionary spending: Some quick hits

Just seeing your discretionary expenses laid out before you can prompt you to make some swift and worthwhile savings. In these days of automated bill payments, it’s easy to miss just how much you’re paying for some goods and services. And simply reviewing them can have you questioning whether you’re getting value for money.

Here are some to look out for, regardless of how you pay for them:

- Cable TV — Packages typically run from $60 to $190 a month. Do your viewing habits justify that?

- Electricity — The Energy Information Administration reckons the average American household spent $111.67 a month on electricity in 2017. Could you try being greener by turning off more lights and switching off appliances when they’re in standby mode?

- Gas — You may not be ready to switch to an electric car. But the Department of Energy says, “On average, it costs about half as much to drive an electric vehicle.” And you may at least want to consider switching to a more fuel-efficient one when you next change

- Newspapers and magazines — For example, it costs $9 a week to get The New York Times delivered, depending on where you live. But an online subscription comes in at $1 a week for your first year

Nobody’s saying you’re wrong to spend as much as you do on these things — or on anything else. If you watch a lot of television, $2,280 a year ($190 a month) may be a fair price to pay for your viewing. And if you love your 2008 Hummer H3 (13.8 average MPG), you may be more than happy when you pay to fill it up. What you’re looking for are items that cause you to exclaim, “How much!?!,” possibly with an expletive in there somewhere.

Discretionary spending: “walking-around money”

We suggested that you start out tracking every cent you spend. But that can be quite a chore. So you may prefer to stop sweating the small stuff, once you have your high-definition picture of your spending.

Instead, you can allocate yourself “walking-around” money, which is also known as street money. In effect, it’s a bit like a pocket money allowance you might give your kids. And it’s intended to cover similar stuff: incidental expenses and little treats.

Many find it helpful to use cash for their walking-around money. You set yourself a limit for the week or month and withdraw that much from an ATM. Of course, you may have the luxury of going back to an ATM to take out more. But that should prompt you to ask yourself why you’re doing that: Were there exceptional circumstances or are you overspending?

Your walking-around money becomes a single line in your budget and it replaces all the lines you’d otherwise need for every candy bar, beer, or pack of gum you buy.

How to Set Up a Budget: Your Technology Choices

There are four main “technologies” from which you can choose when you set up a budget:

- Pen and paper

- A spreadsheet

- The envelope system

- A smartphone app

The app is by far the least labor-intensive. But the others have advantages. Because you can’t manually maintain a budget without carefully thinking about what you’ve spent and earned.

Pen and paper

If you want to be completely “hand-on,” you can buy one of those old-school ledger books that come with pre-lined rows and columns. The left-hand column is for the date and the next (wider) column is for a narrative that describes the expenditure (“Nikes for Billy,” say, or “Walking around money”). You head each column with one of your fixed and discretionary spending categories and the last one is for totals.

For each item of expenditure, you write in the date, your narrative, and drop the amount spent in the appropriate column for that category of expenditure and also in the totals column. At the end of the month, add up all the columns and you’ll see exactly how much you spent in each category — along with your total expenditure. You can check your math by adding up all the category totals and seeing that sum tallies with your totals-column’s total.

You can list your income sources on the facing page.

Your ledger is a statement of your household accounts rather than a forward-looking budget. But it’s great for your identifying possible savings and then setting future spending targets for particular categories of expenditure.

Spreadsheets

You can set up a budget spreadsheet yourself. Simply recreate the written ledger in an electronic format. The advantage is, your computer will do the math for you.

But it’s easier yet to download a spreadsheet that’s been pre-formatted as a household budget. Simply search for “downloadable household budget spreadsheet templates.” You should find quite a selection, some of which are free. Check out a range to choose one that suits you.

Look out for Google Sheets, PearBudget, Vertex42 and It’s Your Money.

Easy-peasy: the envelope system

Dave Ramsey is a big advocate for this system. When you get a paycheck, you leave in your checking account enough to cover those bills you pay automatically or by card. You transfer into a savings account the sum you’ve decided to save. And you withdraw in cash the amount you plan to spend in other discretionary categories.

You then break down your cash according to your spending targets, putting the appropriate amount in each of a series of envelopes upon which you’ve written the discretionary spending category. For example, you might put $300 in your Groceries envelope.

When an envelope’s empty, that’s it. You can’t spend any more in that category without raiding another envelope. And your bills are paid and your spending target met.

Apps

Most young adults prefer to set up a budget online. These apps really can do the donkey work for you. You can link some to all your debit and credit cards. And you can set targets for spending categories. When you overspend, you’ll get an alert telling you what you’ve done.

Different apps are better suited to different needs and personality types. And some are easier to use than others. So be ready to check out a number before you decide on one. For the best functionality and features, you may have to pay a subscription. So choose wisely.

Some of the most widely recommended include:

- Mint — Market leader and near the top in many reviews

- YNAB — Can mimic the envelope system for plastic

- PocketGuard — Tells you how much you have left after your commitments and savings goals

- Wally — Not the easiest to use. But it’s free

- GoodBudget — Great for couples who share the same budget

Explore these and others fully. There’s an app that’s right for you.

The Bottom Line

Nobody said budgeting was going to be easy. But what worthwhile things are?

When it feels like a slog, just remember: You’re taking back control of your life. At the same time, you’re eliminating money worries, which cause huge stress and place a big strain on relationships. And you’re setting yourself up for more and better possessions and experiences in the future. It really is worth it.

Add a backup for emergencies: Compare personal lines of credit