Tiny Home Dreams Don’t Need Huge Bank Accounts

Tiny homes are increasingly popular in the U.S., especially in areas where housing is very expensive. Students, freelancers, and retirees are among those jumping on the trend because they appreciate the lower cost to buy and own. In addition, smaller homes mean less maintenance and cleaning time. But tiny homes are not- popular with mortgage lenders. Personal loans for tiny homes fill that gap.

Personal Loans for Tiny Homes: How Much Can You Spend?

How much can you borrow when you buy a tiny house? As much as a lender is willing to lend. While many top out their loan amounts at $35,000 to $40,000, some personal loan sources finance up to six figures.

The average cost of a tiny home that you build yourself is about $23,000, according to the Spruce. Double that if you want one already built.

Your borrowing limit depends on your credit rating because that drives your interest rate. The better your credit, the lower your rate. The lower your rate, the more you can borrow at the same payment. Your income and other debts also come into play. Lenders consider your debt-to-income (DTI) ratio when you apply for a personal loan. The less you’re spending on other items like credit card payments, auto financing, rent or mortgage, student loans, and other accounts (but not living expenses), the more you can borrow.

Related: Complete Guide to Personal Loans

Your Debt-to-Income (DTI) Ratio

Most lenders prefer a maximum DTI of 36% to 43%, but some will go as high as 50%.

You calculate your DTI by dividing your total account payments and housing costs by your gross (before tax) income.

Suppose that your total household income equals $7,500 per month. And that you have these payments:

- Auto loan 1: $300 per month

- Auto loan 2: $200 per month

- Credit card: $100 per month

- Student loan: $600 per month

And you pay $2,000 a month in rent, but that will go away after you buy the tiny home. So that debt needn’t be counted. However, if you’ll be renting a site for your home, that rent will count in your DTI.

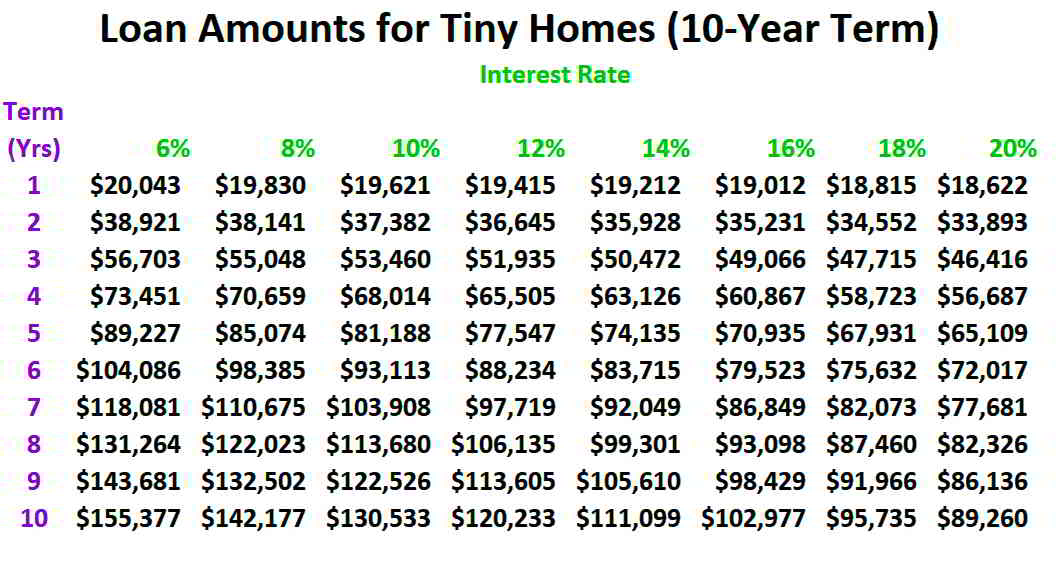

Assuming that you’ll pay $300 a month to rent your tiny home site, your total debt service would be $1,500 a month. $7,500 * .43 = $3,225. And $3,225 – $1,500 = $1,725 available to repay a personal loan.

The table below shows the loans amounts you could finance at different terms and interest rates at that $1,725 payment.

Personal Loans for Tiny Homes: What Is the Payment?

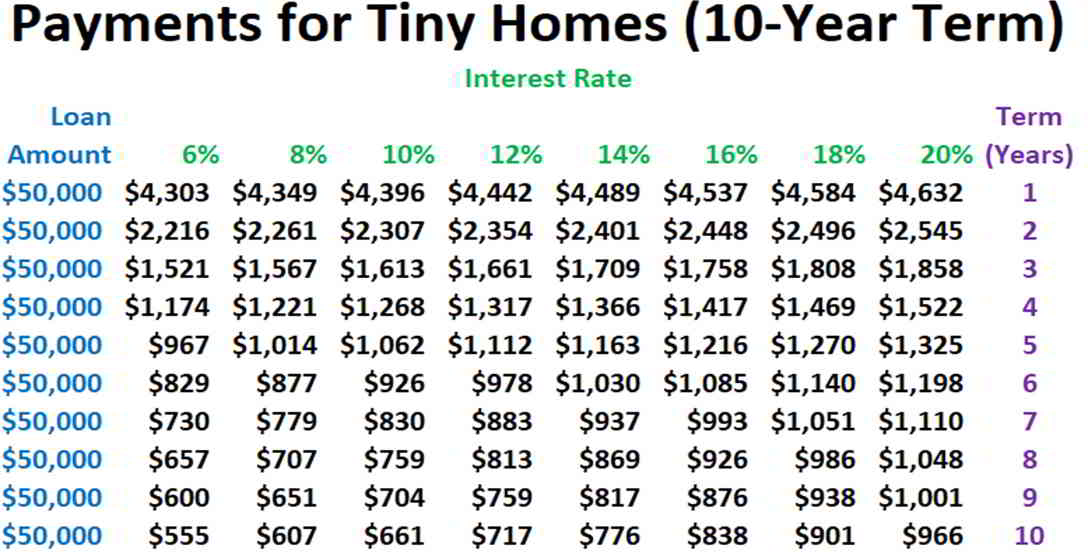

Personal loans don’t come with 30-year terms like mortgages. Many run from one year to five years. Some lenders offer terms as long as ten years. The table below shows the range of loans amounts available for different interest rates and loan terms with a payment of $1,725.

So if you could spend $1,725 a month on a personal loan payment, and wanted to buy a tiny home for $50,000, you could have your loan paid off in about three years. Or you could obtain a lower payment by choosing a longer repayment term.

The table below shows how the repayment term affects your monthly payment if you borrow $50,000:

When comparing personal loan options, choose the combination of the loan amount, payment, and term that works best for you. If you need a lower payment when you first buy your home, pick a longer term. You can always accelerate your repayment when you have more money to spend.

Related: Personal Loan Interest Rates: How to Pay Less

Personal Loans Are Not Mortgages

Just because you use a personal loan to buy a tiny house doesn’t make it a mortgage. That is because mortgages, like auto loans, are secured loans. While personal loans are unsecured loans. Secured financing means the lender can repossess your property — for example, the car or house — if you fail to repay on time.

But personal loans are unsecured. Personal loan vendors don’t care what you spend the money on, because they can’t repossess it anyway. This can save you a lot of the closing costs associated with traditional real estate. You don’t need a home appraisal or title insurance, for one thing. Those items can add hundreds or thousands to the cost of financing a home.

The lender can’t take your tiny house away if you don’t repay a personal loan. But it can take you to court and sue you for repayment. Your credit rating will suffer and you could even be forced into bankruptcy. You can’t just walk away from an unsecured loan, so only borrow what you can afford to repay.

Qualifying for a Tiny House Loan

Lenders consider your income, source of income, and credit when deciding if you qualify for a tiny home loan. If your credit rating is poor, you probably won’t qualify to spend as much as someone with the same income but excellent credit. And your interest rate will be higher, which also cuts the amount you can borrow. But lenders specializing in tiny house loans for poor credit applicants are out there. Expect to pay up to 36% for the privilege of borrowing.

Personal loan underwriters also consider your income and source of income. It must be sufficient to cover your new loan, your other debts, your taxes, and living expenses. And it must be stable and ongoing. So odd jobs probably won’t qualify you. Lenders prefer business income with a solid track record or a steady job in a healthy industry. Job hoppers make lenders nervous.

Personal loans make homeownership possible for those who can’t pay cash for a tiny house or afford a mortgage on a traditional home in an expensive location.