Timeshare Tempting You? Think Twice Before You Borrow

Timeshares have a checkered reputation, largely due to the infamous strong-arm sales tactics employed by many resorts. Timeshare communities want to make it easy to purchase on impulse, so they offer fairly easy credit terms. You can finance a purchase right there in the sales office — but it may come at a steep cost. A personal loan for timeshare may be a better way to buy your next vacation.

Financing a timeshare

When you’re caught up in a timeshare presentation and hyped to buy, the convenient developer financing may be tempting. In fact, the salesperson may present timeshare loans as the only financing option. But it’s smarter to secure financing beforehand if you’re serious about buying a timeshare.

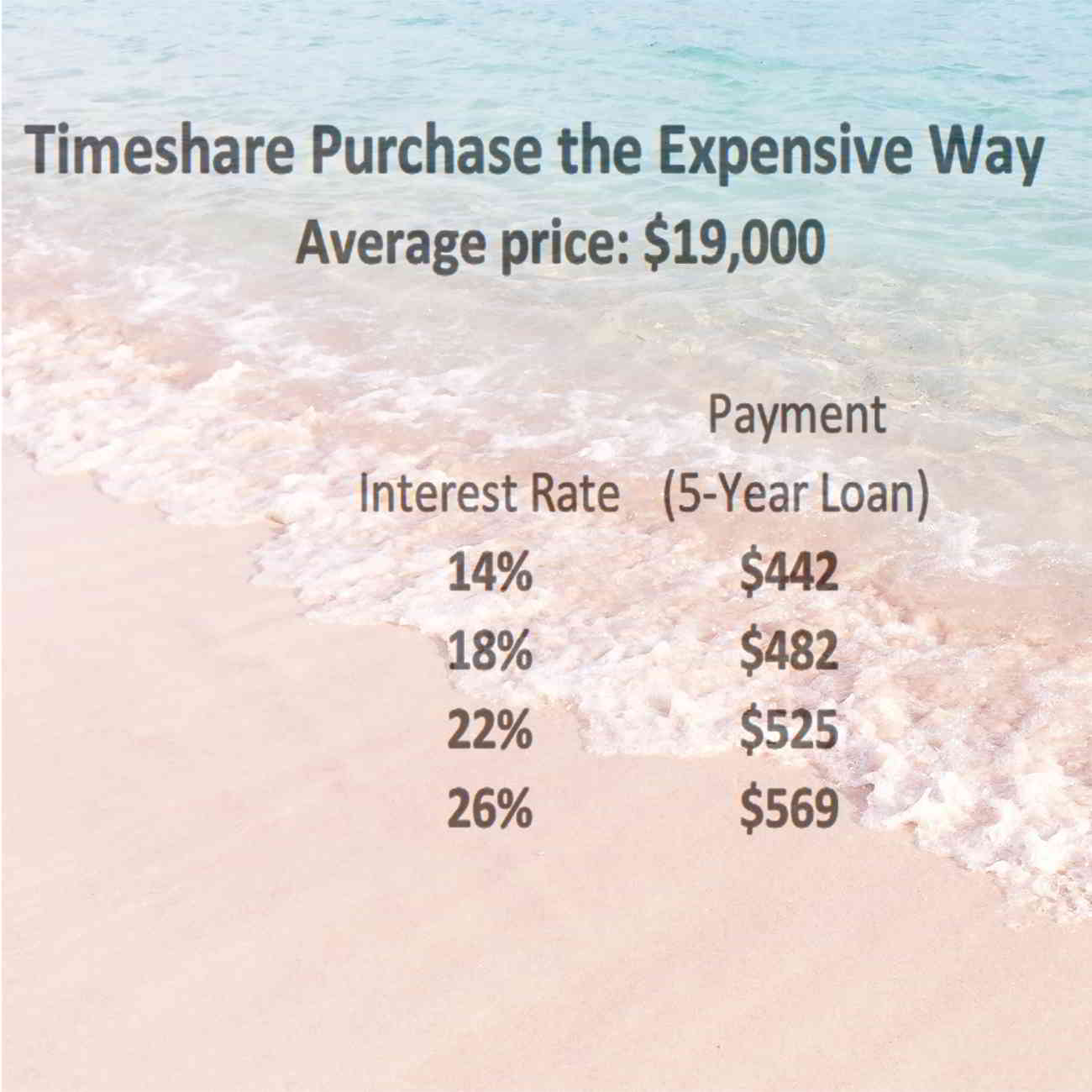

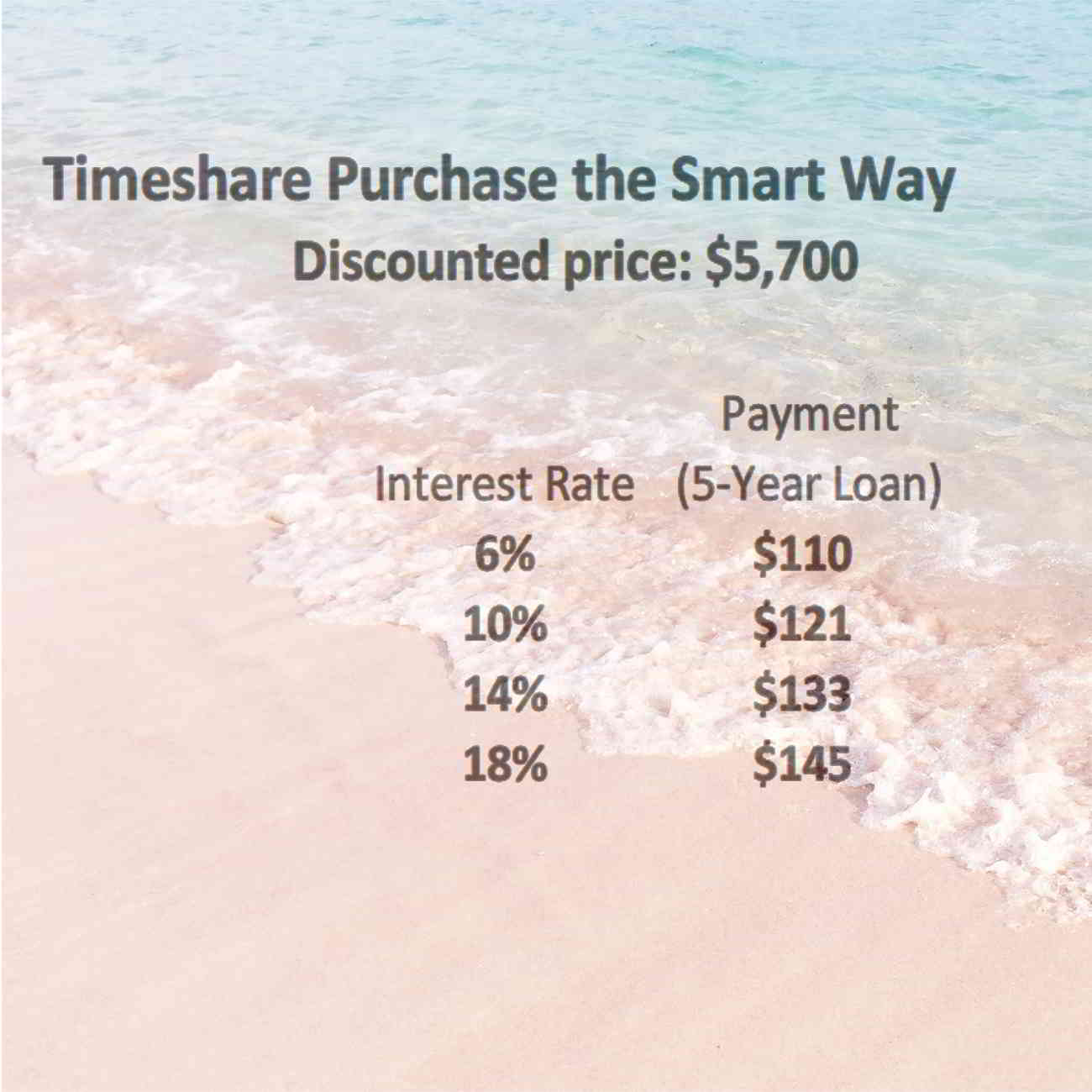

Typically, developer financing interest rates run between 14% and 20%, but can go as high as 36%. You may do much better by borrowing with a personal loan for timeshare purchase — for the most credit-worthy buyers, the interest rate starts at about 6%.

Timeshare purchase: the wrong way

The standard sales strategy for timeshares typically involves tempting prospects with a gift and then subjecting them to a hard sell. The hard sell scheme works because timeshares are usually impulse purchases. Because of the high marketing and commission costs (as much as 55% of the purchase price), buying a new timeshare from an operator is the most expensive way to acquire one.

And, says Forbes magazine, buying at the source gets even more costly when you accept the company’s easy, convenient — and expensive — financing.

“Often, the developer will arrange financing for you, but at a much higher interest rate than banks that do make the loans. What’s more, usually in a foreclosure, the outstanding mortgage balance and the unpaid maintenance fees are higher than the timeshare’s value, which creates what is called a deficiency. Then, lenders can go after your other assets.”

So, purchasing at the source often means paying thousands more than necessary and then financing at a high interest rate.

This doesn’t mean timeshares are a bad idea. It just means you should not purchase them on impulse.

Related: What Is a Personal Loan, Unsecured Loan or Signature Loan?

Buying a timeshare the right way

Many people who purchase timeshares on impulse find they don’t use them as much as they’d expected. Or the annual maintenance fees (averaging $980 a year for a one-week vacation) become too burdensome. They then resell them at a steep discount.

While the average new timeshare cost has hit $19,000, resale properties typically sell at a 45% to 70% discount. The only real reason to opt for a direct purchase, says travel blogger Edward Pizzarello, is to get booking priority if the project is in high demand. Otherwise, you’re better off buying a steeply-discounted resale offering.

Even more important, purchasing on the secondary market means you won’t be buying on impulse. You’ll have time to consider whether you’ll really use a timeshare, and you can take the opportunity to compare resorts and choose the best one for your vacation style.

Related: Personal Loans: Your Complete Guide to Borrowing

Make sure a timeshare is right for you

Experts say that if you prefer to change up your vacations, backpacking one summer, road tripping in the spring and hitting the beach the next time, a timeshare might be too confining for you. But if you like to return to “your place” year after year, a time share offers the advantages of a vacation home at a fraction of the cost.

Budget annual costs

Understand that the purchase price is not the only cost of timeshare ownership. You’ll also pay annual maintenance fees, which average about $980 per year and increase about 3% annually. And don’t underestimate the transportation and other vacations costs you’ll incur every year.

Different timeshare forms

There are four main forms of timeshare ownership, and some are more advantageous for buyers.

1. Fixed Week

You buy the rights to a specific unit in the same week every year. So you know you will always have your unit at a certain time, but you sacrifice flexibility. If you buy a high-season week in a desirable location, you may be able to rent it out when not using it.

2. Floating

You reserve your time during a given period of the year. You get more freedom, but it can be difficult getting a prime time, especially if you did not buy direct and the other owners get first crack at the calendar.

3. Right-To-Use

This allows you to lease the property for a given amount of time each year for a specified number of years. The developer maintains ownership of the property, however.

4. Points Club

With this structure, you can stay at different resorts and different times. Your options depend on the value of the unit and week you purchase — you’re assigned a certain number of points based on that value, and you can use the points to purchase time at other resorts. You can also purchase additional points from the developer.

Related: Personal Loan or Personal Line of Credit? Which Is Right for You?

Understand your rights

Many state laws include generous protections for timeshare buyers, including a cooling off period or rescission period. This period allows you to cancel the transaction for any reason during a specified number of days after your purchase. The rights you get depend on the state in which you purchase your timeshare. You have more protections if your unit is part of an owner’s club or association. It’s like a condominium HOA for owners.

Be wary of any company that requires you to sign the contract documents in a different state than where you plan to buy. They may be trying to skirt that state’s protections for buyers.

Most timeshares in the U.S. get you a deed to a property, called a “timeshare estate.” This usually allows you to rent your week out, sell it or exchange it, and pass it on to your heirs. If you don’t make your maintenance payments, the timeshare company can foreclose

Most others outside the U.S. (for example, Mexico) grant you a “timeshare license” or “membership” which is just a “right-to-use” and may have other restrictions. And if you sign a contract outside the US, you are not protected by U.S. laws.

Know that timeshares are not really investments

The decision to buy a timeshare should really depend on how it will enhance your lifestyle. Don’t make the mistake of considering it an investment. Timeshares don’t generally increase in value. In fact, the secondary market is full of discounted units.

Timeshares are not easy to sell and may not be easy to rent, either. Don’t include potential rentals in your ownership plan unless you buy a high season week in a very desirable location.

Timeshare pros and cons

About one in 12 Americans owns a timeshare, according to the American Resort Development Association. And for many, timeshares provide a family vacation experience similar to that of owning a vacation property — for a lot less. The facilities are usually much nicer than those of comparable hotels in the same price range, and they are widely available in some of the most desirable vacation spots in the world. You may be able to trade weeks and enjoy prepaid vacations around the globe.

But timeshares can also lock you into a plan that may not work for you in the future. And you may not be equipped to cover the increasing maintenance costs each year. It’s a highly individual decision.

The main takeaway, however, is that there is an expensive way and a discounted way to purchase timeshare property. And if you choose to buy timeshare property, the personal loan for timeshare purchase is an option that should not be overlooked.