Summer’s Hot but So Is Your Credit Card Bill

A recent survey by AmONE found that most consumers spend more during the summer. Higher temperatures and sunny days are enticing incentives to have fun — at the beach, on vacations, in the movie theater, and elsewhere. Many cover additional summer spending with personal loans, credit cards, savings, or budget sacrifices.

70% spend more during the summer

Higher temperatures and sunny summer days are enticing incentives to have fun — on the beach, via vacations, at the movie theater, and elsewhere. It’s no surprise, then, that many consumers engage in extra summer spending, according to the 543 survey respondents.

- Only 8% said that their spending did not increase

- Just under one-third (29%) increased their spending by $500 or less

- Most (37%) spent an extra $500 to $2,000 over the summer

- One fourth (26%) spent more than an additional $2,000 during the summer

Of those who spent over $2,000 for summer extras, 41% went much further — spending more than $5,000 for summer-related activities.

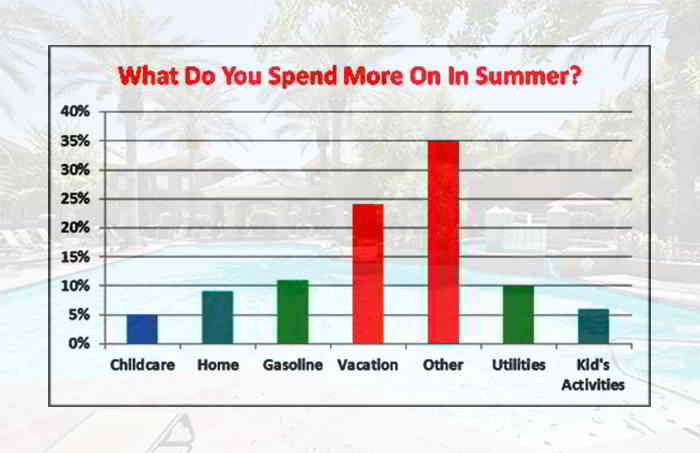

The hot dog days of summer

Most families experience traditional extra summer costs, from air conditioning to summer camp. Here’s the breakdown:

- Vacations and travel (22%)

- Gasoline (11%)

- Utilities (10%)

- Home improvements (9%)

- Childcare (6%)

- Children’s activities (5%)

- Other, including ballparks and hot dogs (36%)

Nearly half (48.7%) said that they covered most of these extra costs by pinching pennies elsewhere, and 15.1% indicated that they used savings for summer spending. But everyone else resorted to some form of borrowing (17%) or found another way to make the extra money — perhaps by working longer hours or holding garage sales.

Big spenders more likely to borrow

It’s understandable that those whose summer spending increases the least would have an easier time fitting the extras into their existing budgets without borrowing.

While 11% of those spending between $500 and $2,000 on summer activities took loans or tapped credit cards, nearly four times as many (43%) of those who spent more than $2,000 financed their summer costs. For these larger amounts, personal loans can be a better deal than credit cards.

Summer spending adds up

Richard Barrington, senior financial analyst for MoneyRates.com, says these survey results make sense.

“People are much more active in the summertime because the weather is more conducive to travel and making outdoor plans. Plus, families with kids out of school on vacation need to find ways to keep those kids busy,” he says.

Michelle Wilfer, branch manager for Collins Community Credit Union, agrees.

“I am not surprised by these poll findings based on what our members state when they come in for loans and credit cards during the summer,” she notes. “It’s not uncommon for our members to request personal loans for vacations or home improvement projects.”

What summer spending pays for

Beverly Friedmann, who lives in New York City, says she plans to spend an extra $3,000 this summer on several things she probably wouldn’t buy during other parts of the year. These include travel and vacations, clothing, home goods, and leisure activities.

“I maintain a savings fund to pay for these extra summer expenses,” says Friedmann. “I save throughout the year and am generally quite frugal, so the summer feels like quite a treat.”

Calvalyn Day from Indianapolis, meanwhile, likes to splurge on enrichment activities with her kids in the summer months, when she works from home. She’s able to afford these seasonal purchases — which equate to around $1,500 — by cutting back on spending in other categories.

“I’m mindful of how we use the existing budget. I might take some money from our food budget to contribute to a summer entertainment purchase, for example,” notes Day.

Gina Pogol, personal finance expert and spokesperson for AmONE, does not recommend long-term financing for short-term purchases. “You don’t want to be paying for this summer when next summer comes around.”

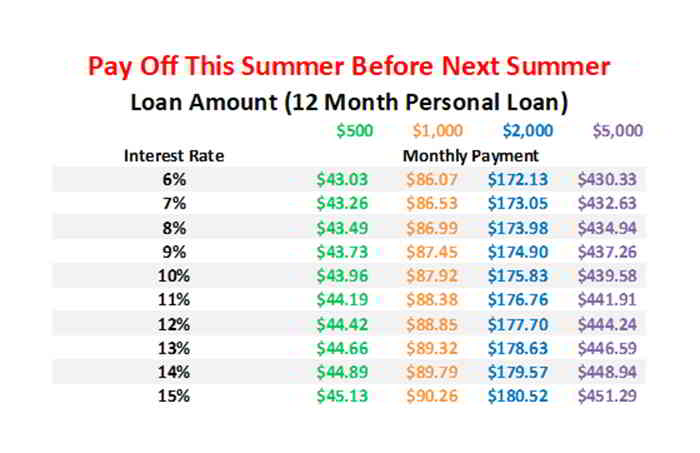

The chart below shows what it would take to pay off a personal loan at varying amounts and interest rates.

Borrowing to fund your summer fun

The experts say borrowing cash to pay for extra summertime expenses isn’t necessarily a bad idea.

“If you need to get your hands on some extra cash this summer, and your credit is in decent shape, consider applying for a credit card with a 0% introductory purchase APR offer. With this option, you can carry a balance over a certain period of time without ever incurring a penny of interest,” says Sean Messier, credit industry analyst.

“Introductory APR periods stretching well over a year are quite common. You just need to ensure you’re able to pay off all the debt you accumulate before this intro period ends.”

However, many don’t qualify for or take advantage of low APR credit card offers. Instead, they ring up charges on a card that may carry high interest rates. That’s why personal loans may be a better option.

Personal loans and other financing

“The problem with a lot of summer spending is that it’s spontaneous. And lack of planning can cause financial problems,” says Barrington. “Using personal loans is generally cheaper; per the latest Federal Reserve figures, the average credit card balance is assessed interest at the rate of 17.14%, compared to 10.63% for the average personal loan.”

If you have home equity, a home equity loan or home equity line of credit (HELOC) are two other borrowing options. However, these loans can take time to set up, and the costs can be prohibitive if you’re just trying to get a couple thousand dollars for a vacation.

“I wouldn’t recommend that a consumer use the equity in their home to finance summer expenses unless they are for home improvements,” cautions Wilfer, who notes that interest rates for either average around 6% at her financial institution.

Gina Pogol says that there are exceptions to most personal finance rules. “Summer spending is a highly-individual decision,” Pogol explains. “Your children may be Disney-aged only once, and you might want to finance those memories before they become teenagers. How much you spend, and how you get the money depends on your priorities, your resources, your family’s traditions and your financial stability.”